The Federal Reserve’s Toolkit: How Interest Rates Dictate Your Lifestyle

Discover how the Federal Reserve's toolkit shapes your daily life. Learn how the Fed affects the stock market and what 2026 interest rate trends mean for your wallet.

If you’ve ever felt like a tiny boat tossed around by the waves of the global economy, the Federal Reserve is the moon controlling the tides. While most people think of the Fed as just “the group that changes interest rates,” they actually wield a sophisticated toolkit designed to keep the U.S. economy from either freezing over or catching fire.

As we move into early 2026, with the Federal Funds Rate sitting in the 3.5% to 3.75% range, understanding these tools is no longer optional—it’s a survival skill for your finances.

The Federal Reserve’s Power Tools

The Fed doesn’t just have a single “interest rate” button. They use a combination of levers to influence how much money is flowing through the system:

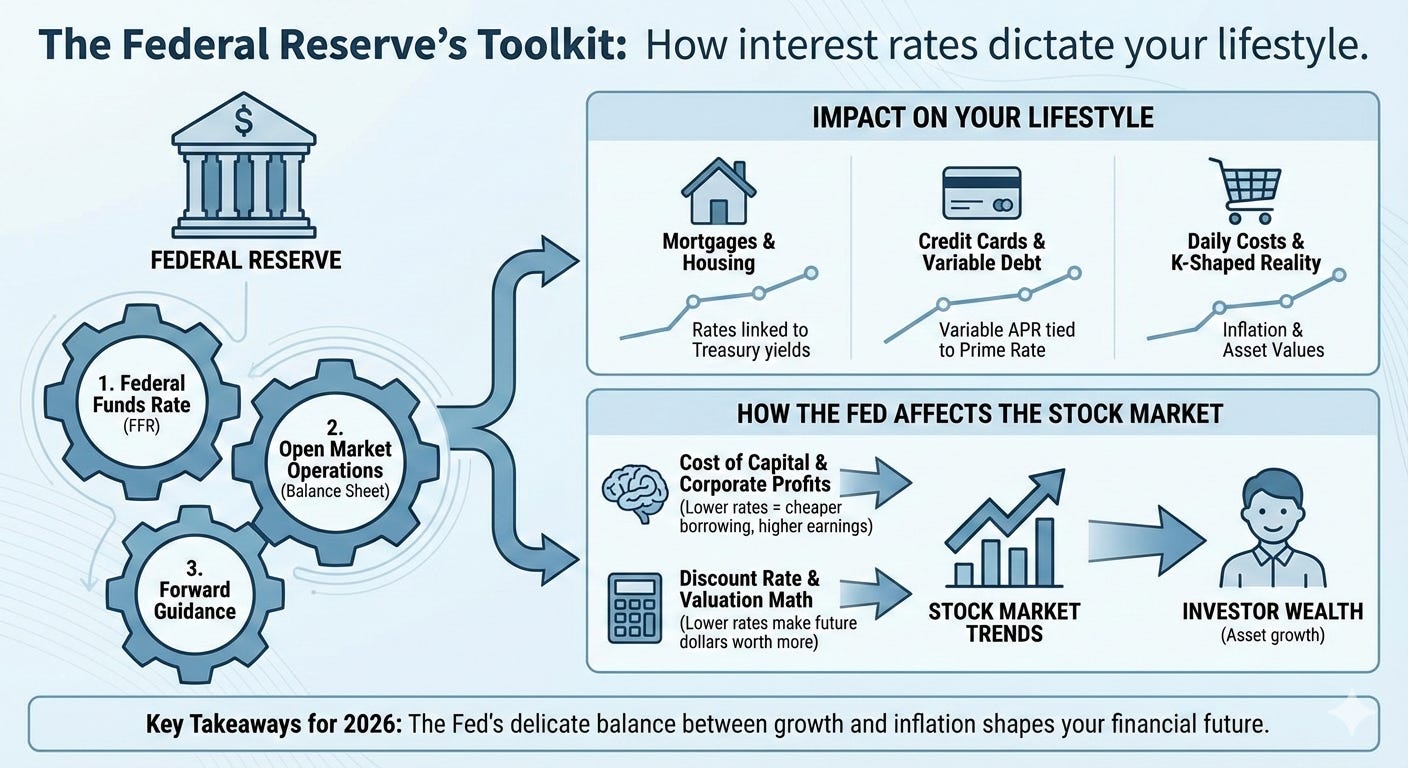

The Federal Funds Rate (FFR): This is the “Godfather” of rates. It’s what banks charge each other to lend money overnight. When this goes up, it becomes more expensive for your bank to do business, and they pass those costs directly to you.

FOMC - Open Market Operations (The Balance Sheet): The Fed buys and sells government bonds. Buying bonds pumps cash into the economy (easing); selling them sucks cash out (tightening).

Forward Guidance: This is essentially the Fed “talking” the market into a certain mood. By telling us what they plan to do in late 2026, they influence long-term mortgage and auto loan rates today.

How the Fed Affects the Stock Market

For investors, the Fed is the ultimate trendsetter. How the Fed affects the stock market comes down to two main factors: The Cost of Capital and The Discount Rate.

Corporate Profits: When the Fed keeps rates lower, companies can borrow money cheaply to expand, hire, and innovate. This usually leads to higher earnings and, consequently, rising stock prices.

The Valuation Math: Investors use a “discount rate” to value future company earnings. When interest rates are low, those future dollars are worth more today. This is why “growth” and tech stocks often skyrocket when the Fed signals a dovish (lower rate) stance.

The Yield Chase: When the Fed lowers rates, boring “safe” investments like CDs (certificates of Deposit) and Savings Accounts pay less. This forces investors to move their money into the stock market to find a decent return, driving prices even higher.

From the FOMC (Federal Open Market Committee) to Your Front Door

The Fed’s toolkit doesn’t just stay on Wall Street; it lives in your wallet. Here is how their 2026 strategy is currently dictating your lifestyle:

Mortgages & Housing: Even though the Fed doesn’t set mortgage rates, they move in tandem with the 10-year Treasury yield, which is heavily influenced by Fed policy. If you’re looking to buy a home this spring, you’re essentially betting on the Fed’s next move.

Credit Cards & Variable Debt: Most credit cards have a variable APR tied to the Prime Rate. When the Fed cuts by 0.25%, your interest charges eventually drop, too. It’s a slow win, but a win nonetheless.

The “K-Shaped” Reality: In 2026, we are seeing a “K-shaped” impact. Those with assets (stocks and homes) are seeing their wealth grow as the Fed supports the market, while those relying on wages may still be feeling the pinch of persistent inflation in groceries and rent.

The Bottom Line for 2026

The Federal Reserve is currently walking a tightrope. They want to support GDP growth without letting inflation creep back above 3%. Whether you are a day trader or just someone trying to pay off a car loan, you are playing in a stadium designed by the Fed.

Keep your eyes on the “Dot Plot” (future interest rates projections) and the FOMC press conferences. In this economy, the Fed isn’t just a central bank—it’s the architect of your financial future.

Disclaimer:

The information provided by The Market Dispatch is for educational and informational purposes only and should not be construed as financial, legal, or investment advice.

The Market Dispatch, its authors, and contributors are not financial advisors, brokers, or attorneys. Any opinions, analyses, or projections expressed are solely those of the authors and do not constitute specific recommendations for any individual.

Investing involves risk, including the potential loss of principal and capital. Past performance does not guarantee future results. Before making any financial decisions or investments, you should consult with a qualified financial advisor or other professional who understands your personal circumstances.

By reading this newsletter or using any related materials, you acknowledge and agree that The Market Dispatch and its team will not be held liable for any loss, damage, or expense incurred as a result of reliance on the information provided.

The Fed does show up in many places in a person’s life.

And considering how the market has run, we see the K-shaped split between asset owners and wage earners.

Godfather of rates. I think there's more room, but I understand the tightrope.

With new FOMC voters, I do await the Dot Plot at the next meeting. Initially, I would expect the new members to be more hawkish.